If you’ve had any experience in some of Sydney’s Western Suburbs you’d quickly understand that perhaps the state of our housing market isn’t as good as it’s cracked up to be. I remember meeting a couple in their just completed brand-new house, in a ‘new town’ located about 70kms south west from the Sydney CBD, which was being offered for sale cheaper than you could build one next door. Alarm bells yes but professional concern no, as on a higher level we avoid these areas when it comes to investment. In my experience the last places to rise in value become the first to fall, so when looking for a stress free and steady growth path, these areas aren’t highlighted on our radar.

The other far greater concern for me has always been debt levels and the ability to service that debt. No doubt much of the inflation in house prices has been due to the last few years of lower than usual interest rates, bolstered by a boom market locally and the resulting gold rush of home owners and investors into the area.

Mortgage debt is high, incomes don’t necessarily match and worse still consumer lending is on the rise with credit companies, whether in the guise of store or credit cards, handing out accounts like candy to kids at Halloween to all and sundry. To add to this the cheaper rates for car finance and the perceived inflated equity in the homers of borrowers have put a brand-new ute/station-wagon/sedan/4WD/hot-hatch/caravan in the drive way and no doubt there’s been a holiday or two.

I’ve been highlighting this debt disparity for a while, so my ears always prick up when the smart people at research houses rattle their phones and get feedback from the populous that resonate with my concerns.

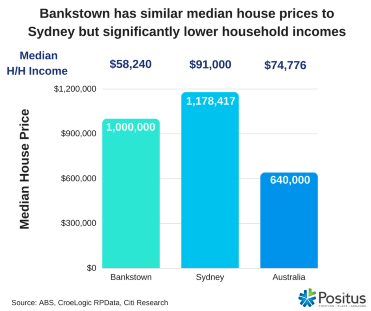

Recent findings from some of these fellows with sharpened pencils at Citi Research highlighted just that. Their trend setting target was Bankstown, a suburb only 20kms from Sydney’s CBD where the income to house price ratio is currently 17.2% as opposed to Sydney at 12.9%. Just for the record the median household income in Bankstown is $58,240 a year, 36% below the Sydney average and surprisingly 22% below the countries national average. Median house prices here are $1M, just 15% below the Sydney average of $1.2M and the national average of $640K.

So where does this lead us, or more accurately… interest rates have got to rise eventually, then what?

Before I continue I must expand on the word ‘Decimation’, a favourite of mine with origins from Roman times.

Decimation was a form of military discipline used by senior commanders in the Roman Army to punish units or large groups guilty of capital offences, such as mutiny or desertion. It is derived from Latin meaning "removal of a tenth", where the killing of one in every ten of a group of people as a punishment for the whole group.

Decimation; casualties everywhere and many that perhaps shouldn’t have got caught up in it in the first place. As for a ten percent cull, alas in this case I think it will be worse.

More recently I was talking to a well-known Sydney developer, who after their pipeline of sales had slowed down on a project some 20kms north west of Sydney, was quizzing me about strategies to help him move more stock. Rather than tell him that the market just didn’t need any more overpriced, high rise dog boxes, I thought it prudent to take a different tack by mentioning he should look at his target market within the local demographic to see if they could afford their product using the major banks lending criteria. Of course, the numbers didn’t match (even without the APRA imposed stress tests) and the best strategy available was to (stop being greedy and) reduce his prices by 20%. Off course that advice fell on deaf ears but at least allowed me to politely leave the room without telling him what I really felt about his overpriced, badly designed and located property.

Another thing we should throw in the ring to add to this impending issue is geography. In that I mean location, specifically accessibility to good jobs, amenity and infrastructure. Whilst the areas highlighted have a bit going for themselves they really aren’t anything like Sydney, with employment and services by no means on a level with the great city. So why then are these areas bundled it into the ‘Sydney’ bracket?

I strongly believe that a bit of ownership needs to take place. We desperately need to rid ourselves of the naming of the everlasting suburban sprawls and give them new identity, new prospects and new pride. Nodes or sometimes even transport hubs is how modern government describes them but they are worth more than that. Am I alone in thinking this description has connotations of commuter slums built around stations and transport terminus feeding the big cities?

I say build them up sensibly, give them reason to exist, encourage growth and opportunity and the rest will follow. Back in the mother country they’ve been calling them towns for aeons and for every good reason. Every town has pride, which can be both seen and heard in both the accent (or indeed local dialect) and the passion for the local football team. Yes folks, identity goes far and not just down in Australia but all over the world.

Low and behold as I’m pondering this muse a note pops up that the Greater Sydney Commission revealed their ‘draft’ 20-year plan for a sustainable future as Sydney continues to grow. In short, a plan to work out how to employ and accommodate Sydney’s expected eight million residents by 2056, that’s an increase of 817,000 jobs and a further 725,000 dwellings. So here they are with a plan for three cities; the positive that two at least currently exist, the third a mosquito infested packet of land edged between the mountainous national park and current urban splutter and sprawl now increasingly popular with land bankers.

A fifty-year hope and dream some might think. Whilst on the right track, many will agree too little too late and excuse the pun if you include the proposed airport and rail system ‘on a wing and a prayer’. Having just returned from an in-depth tour of the area, one can only hope that the grid like sub-divisions of badly built mini McMansions with their gaudy ‘Colorbond’ fences and severe lack of hedgerows and/or greenery become a thing of the past, as government start to use their heads as to what is unacceptable visual pollution to our once productive farmland and countryside. But hey they’ve screwed it up so far so why expect anything different in the future. I wonder will this new city include anything other than rows and rows of vanilla housing or shall we expect an international competition to design this new city as happened in Canberra in 1911? Sadly we will probably sell ourselves short in a cost saving exercise, and leave it in the hands of our somewhat short sighted councils and developers, then have the money use government to overrule what sense we have left in the tank.

As fifty years is another lifetime for me, moving swiftly forward I suggest government print a large map and get a big fat marker pen to highlight what each area really is. Let the locals create their identity, create industry, create employment and create tribe. Real microcosms in an otherwise barren landscape to take advantage of their corner and separate themselves from the effects of being bundled to close to their bigger brothers.

In the meantime, I’d watch this space. If interest rates move 1% that could amount to an extra $500 per month on a mortgage in Bankstown, which could be tough to handle if the average income is only $58,240 per household and of course not forgetting the extra stress on the credit card and car payments.

Perhaps as I close it’s time to talk about the shortfalls of negative gearing when interest rates increase… but no I will save that for another time as todays muse is all about limits.

On that note, when interest rates rise I will then know where my city limit is, as I will be crossing it to buy my next heavily discounted second-hand car.